- Printed Journal

- Indexed Journal

- Refereed Journal

- Peer Reviewed Journal

E-ISSN: 2617-5762|P-ISSN: 2617-5754

2018, Vol. 1, Issue 2

Forecasting of Maruti Suzuki returns using ARCH/GARCH model

Ramita

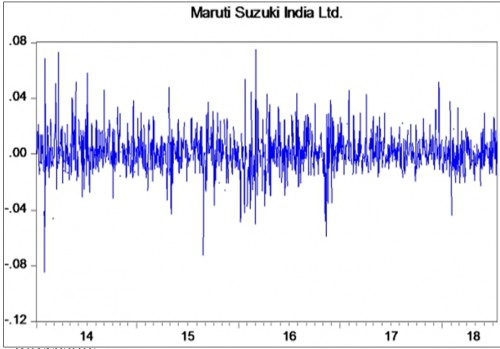

Time Series Modelling has been used to forecast the returns of Maruti Suzuki Ltd. The order of the best ARIMA Model has been found (1,0,2) for estimating the Mean Equation. After estimating it, it has been found that heteroskedasticity effect was present and Hence, Variance equation has been estimated using ARCH/GARCH Model. The graphs of returns of Maruti Suzuki Ltd has been compared with forecasted Maruti Suzuki returnsand data has been showed.

Fig. 1: Mean Equation

Fig. 2: Model Identification

Pages : 24-27 | 2639 Views | 1561 Downloads

How to cite this article:

Ramita. Forecasting of Maruti Suzuki returns using ARCH/GARCH model. Int J Res Finance Manage 2018;1(2):24-27. DOI: 10.33545/26175754.2018.v1.i2a.11

Related Journals

Related Journal Subscription

International Journal of Research in Finance and Management

Copyright © 2024. All Rights Reserved.

Other Journals

Other Journals